Pinewood is poised to wrest market share from industry rivals operating in the UK’s £100 million dealership management system (DMS) market since separating from Pendragon, according to financial services group Zeus Capital.

Since completing its transition into a pure-play Software as a Service (SaaS) entity, Zeus said it saw significant potential in Pinewood’s North American joint venture with Lithia - which has taken a 20% stake in the business – which will help drive the business as a major player in the vast US automotive software market.

Pinewood and Lithia, one of the largest motor retailers in the US, have each invested £10m in the joint venture with perpetual rights to sell the Pinewood product in the North American market.

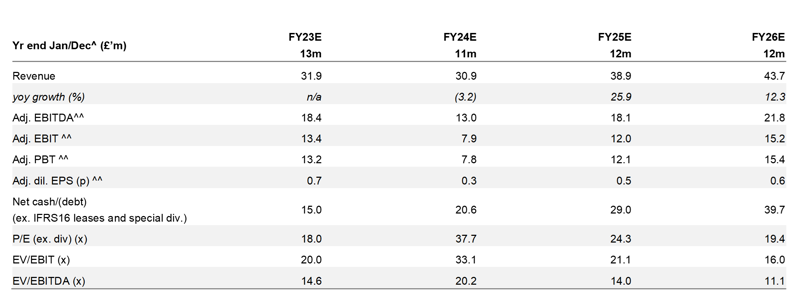

An accelerated growth plan will see Pinewood aiming to grow from its current 33,000 DMS software users to 48,000 by 2027 with its cloud-based solution. Earnings are projected at £27m in that year, representing 59% growth versus an anticipated £17m for the 12 months to December 2023.

While around 2,500 new users will come from deploying the software in Lithia’s 50 UK sites, Pinewood’s integration with 50 vehicle OEMs and partnerships with manufacturers should drive user number growth internationally.

“For example, rolling out the software across all Porsche sites in Japan is expected to add around 4,000 users and is already underway,” said Zeus Capital in a new research paper.

Despite initial development meaning Pinewood's 49% stake's may drop in value, Zeus Capital’s said its forecasts over the next two years reaffirmed its confidence and reiterated the case for investment.

“The potential for Pinewood to expand its user base both domestically and internationally, while maintaining robust EBITDA margins and cash flow conversion, appears promising.”

“Based on the group's targeted FY27 EBITDA of £27m, we project a discounted valuation of 23.7p per share, indicating a potential upside of 93%. Additionally, there exists further growth potential as the North American joint venture solidifies its presence in the expansive US automotive software market.”

Lithia's network of approximately 17,500 users across 300 US dealerships means that if the joint venture captures a portion of Lithia's annual spend of between US$100m-US$150m on DMS, CRM, and tech stack, it could potentially generate earnings of US$60m in the medium term.

AM Dealer Recommended 2025

In this issue we present the top perfomers in the 2025 AM Dealer Recommended research.

Significant motor retail industry suppliers have been endorsed by UK automotive retail leaders in our research programme.

We surveyed dealers from our audience to find out who they trust most and rely on for products and services in a variety of critical aspects of their motor retail operations.

Almost 30 companies received sufficient support from AM's dealer audience to become Dealer Recommended this year.

Find out who they are and learn from them how they can problem solve in your business.

Read now

Author:

Aimee Turner

Deputy editor

AM deputy editor Aimée Turner has been a specialist B2B editor and journalist covering the international transportation sector for more than 20 years.

She has specialised in the significant safety, regulatory, and environmental issues that impact advanced technology businesses in the pursuit of more efficient, safer and sustainable transportation modes.

Login to comment

Comments

No comments have been made yet.