New car sales declined to their lowest February total since 2015 across Europe as Renault’s Clio toppled the Volkswagen Golf from the top of the region’s best seller rankings.

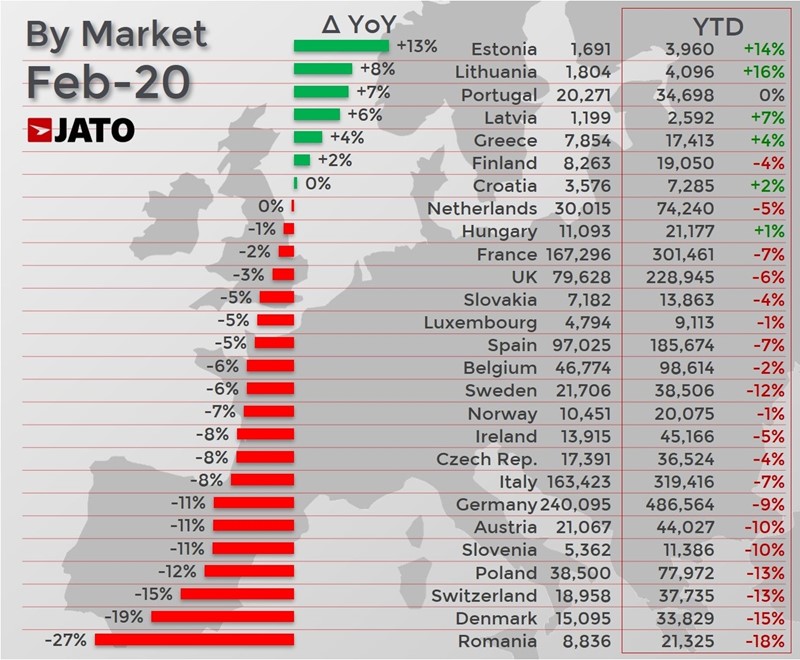

Jato Dynamics revealed in its monthly report on the European region’s 27 car-selling nations that a total of 1,063,264 new vehicles found owners last month, compared to 1,143,852 in February 2019 – a decline of 7% year-on-year and just 11.3% up on 2015’s 955,113 units.

The performance leaves the sector 7.3% down by volume year-to-date, at 2,194,706 units.

Felipe Munoz, global analyst at Jato, said that the situation in Europe’s new car sector was “rapidly deteriorating” – even ahead of March’s escalation of the COVID-19 coronavirus outbreak – due to complex regulation, lack of available homologated cars, and increasing pressure on the economy.

“All of these factors are having a detrimental impact on consumer confidence”, he added.

AFV market share growth

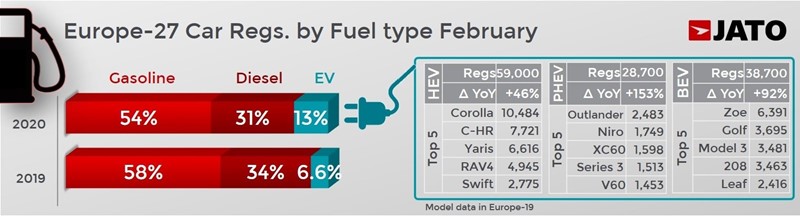

According to Jato’s industry data, alternative fuel vehicles (AFV) were once again delivered growth in February, despite the market’s downward trajectory.

It showed that AFV registrations jumped from 75,400 units in February 2019 to 135,500 units last month.

The increase of over 80% came at the expense of diesel and petrol cars who saw significantly fewer registrations, however.

Munoz said: “So far this year, electrified vehicles have been the only lifeline for manufacturers operating in Europe.

“This is good news, as the industry’s electrification plans have finally seen a positive response from consumers.”

Sales of AFVs more than doubled in Germany and France during February and represented 75% of all passenger car sales registrations in Norway, 33% in Sweden, 31% in Finland, 22% in Netherlands and 17% in Hungary.

Sales of AFVs more than doubled in Germany and France during February and represented 75% of all passenger car sales registrations in Norway, 33% in Sweden, 31% in Finland, 22% in Netherlands and 17% in Hungary.

France leads among the big five markets, with an EV penetration of 14%, against 13% in the UK, 11% in Germany, 10% in Spain, and 8.6% in Italy.

The shift towards AFVs is now starting to place pressure on the previously buoyant SUV market, according to Jato.

Registrations for SUVs fell by 1.7% to 415,300 units last month, taking the year-to-date total to 865,500 units – down 1.4% year-on-year.

Jato said that the fall in registrations was due to the compact SUVs, declining by 3.7% in contrast to the strong growth experienced by large SUVs, who saw an increase of 17%.

Model winners and losers

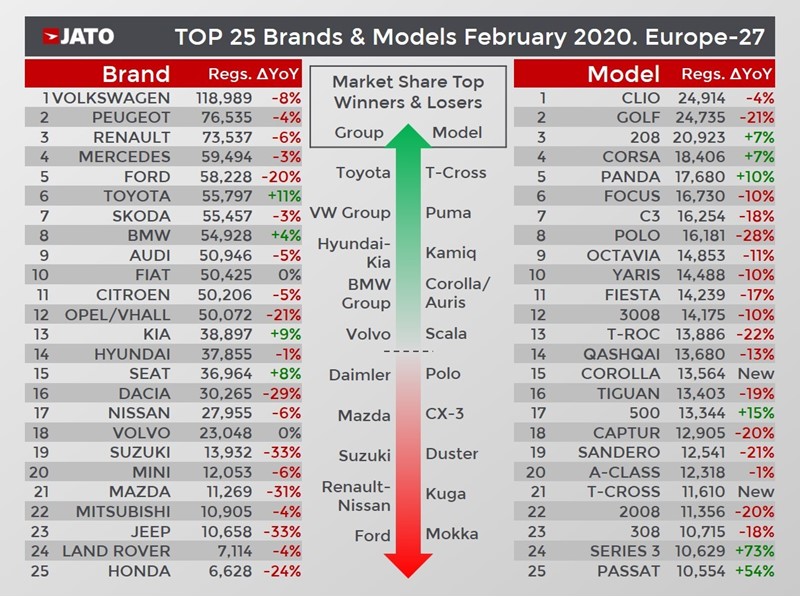

February brought a landmark shift at the top end of the new vehicle sales rankings, with the region’s long-time best-seller, Volkswagen’s Golf, being dethroned by the new Renault Clio.

This was explained by Renault’s new Clio having been available to the market for a longer period of time than the recently-launched eighth-generation Golf.

Other changes within the top 10 best seller rankings included the Fiat Panda hatchback's move into the 5th position, and SUVs' fall from the rankings entirely.

Perhaps surprisingly, mid-size cars posted the highest growth among all segments, thanks to the BMW 3-Series, boosted by the new generation, and the Volkswagen Passat, Jato revealed.

The BMW and VW models’ combined registrations made up 31% of the whole midsize segment volume.

The positive results for midsize cars were not thanks to the Tesla Model 3, whose volume actually fell by 6%.

Across all model types, the European new car markets biggest sales improvements came from: the Fiat 500; BMW 3-Series; Volkswagen Passat; Hyundai Kona; BMW 1-Series; Audi A4; Volvo XC40; and Citroen C5 Aircross.

Among the latest launches, it is important to mention the 13,600 units registered by the British-built Toyota Corolla, 11,600 for the Volkswagen T-Cross, 7,500 units of the Ford Puma, 6,700 units for Skoda Kamiq, 5,100 units for Skoda Scala, and 4,600 units of the Mazda CX-30.

Login to comment

Comments

No comments have been made yet.