The decline in trade values and fortunes on the retail forecourt show no signs of reversing.

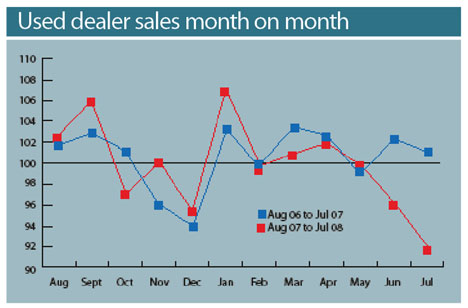

Trade value erosion in particular is well illustrated by Black Book pricing movements between July 2007 and July 2008, compared with the previous year.

The earlier period saw a reduction of 2.7% while in the past year it was 14.3%.

Despite continuing media references to looming recession, there are some contradictory indicators such as May bringing record High Street spending in the midst of ongoing negative comment.

In the used car retail market, there is some evidence that the decline in showroom traffic may have bottomed out – but in parallel with continued reduction in sales.

This suggests that customers may have been returning to the showroom during July at least to browse, if not to buy.

This ties in with reports that consumers are feeling cautious due to economic slowdown warnings rather than unable to purchase for solid financial reasons.

The mood of the market is also illustrated by CAP’s measure of dealer sentiment.

This reveals a stark contrast between last year and this, with the gloomy mood deepening.

Again, the demoralising effect of seeing an increase in footfall but a continued decline in actual sales is illustrated.

Dealer mood is also compounded by the fact that even under ‘normal’ circumstances, a pre-September registrations slowdown would be expected.

This year, however, there seems to be little prospect so far of an uplift at the end of the summer.

production line")

Login to comment

Comments

No comments have been made yet.