The UK automotive sector has reported a return to growth in its most critical month of the year, raising questions over whether this signals the beginning of a long-term recovery – or a temporary reprieve in an industry increasingly vulnerable to global trade tensions.

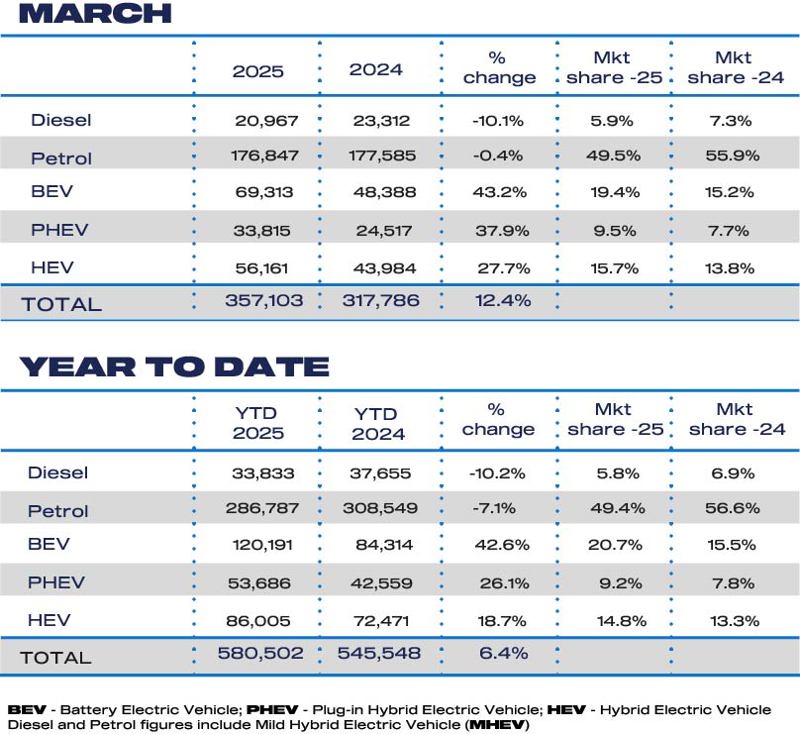

According to new figures from the Society of Motor Manufacturers and Traders (SMMT), over 357,000 new vehicles were registered in March – representing a 12.4% year-on-year increase.

David Borland, EY UK & Ireland automotive leader, responded positively to the figures but warned that wider geopolitical developments could quickly darken the outlook.

- Do the new car registration figures mark the start of a positive trend?

- Or a one-off in an industry under pressure from costs, tariffs and supply chain fears?

- Many companies will be challenged to the limit

The UK automotive sector has reported a return to growth in its most critical month of the year, raising questions over whether this signals the beginning of a long-term recovery – or a temporary reprieve in an industry increasingly vulnerable to global trade tensions.

According to new figures from the Society of Motor Manufacturers and Traders (SMMT), over 357,000 new vehicles were registered in March – representing a 12.4% year-on-year increase.

David Borland, EY UK & Ireland automotive leader, responded positively to the figures but warned that wider geopolitical developments could quickly darken the outlook.

“As the global automotive industry assesses and responds to the US tariff changes, the UK automotive sector returned to growth in the most important month of the year with over 357,000 registrations resulting in a 12.4% year-on-year uplift," he said.

Borland (pictured) highlighted the broader threat of escalating trade barriers, including the recent introduction of US tariffs that could push global automotive businesses into a $1 trillion tariff regime.

Borland (pictured) highlighted the broader threat of escalating trade barriers, including the recent introduction of US tariffs that could push global automotive businesses into a $1 trillion tariff regime.

He added that the UK sector’s hard-won resilience could be tested to the limit in 2025, as tariffs combine with rising employment costs and economic uncertainty.

“The UK automotive sector has shown incredible resilience in the last decade despite facing a variety of headwinds. However, the impact of tariffs and higher employment costs from this April – on top of an already challenging growth and economic environment – is going to challenge many companies to the limit."

A new 25% US import duty, now in effect for all cars assembled outside the US, will extend to car parts from May 3. The consequences for UK exports could be severe: 80% of the UK’s 780,000 cars produced in 2024 were exported, with the US representing the second-largest destination at 17%.

“So far, the impact is being managed by a combination of manufacturers absorbing costs, the supply chain sharing the burden and passing costs to the end consumers. It remains to be seen if this is sustainable, and the sector faces tough decisions if these tariffs stick,” Borland warned.

Fleet and retail sales show growth – but for how long?

Commenting on the March sales split, Edwin Kemp, director at EY-Parthenon Strategy, noted the surprising rebound in private retail demand.

“Much of last year’s growth in new car registrations was driven by a consistent upward trajectory of fleet sales, whilst there were marked challenges for private retail demand. However, the most recent data showed growth across both sales types."

“In March, contrary to recent historical trends, retail sales saw a significant year-on-year increase of 14.5%, with fleet sales also seeing strong year-on-year growth of 11.5%. The real question is whether this marks the beginning of a more sustained positive trajectory, or just a one-off, particularly given the ongoing market headwinds for new car registrations."

Battery Electric Vehicles (BEVs) were another bright spot in March, achieving their strongest uptake on record. But Kemp cautioned that significant structural challenges remain before BEVs can take the lead in the UK’s transition to net zero.

Battery Electric Vehicles (BEVs) were another bright spot in March, achieving their strongest uptake on record. But Kemp cautioned that significant structural challenges remain before BEVs can take the lead in the UK’s transition to net zero.

“On the powertrain transition, whilst March 2025 was the strongest month ever for BEV uptake, the complex combination of affordability challenges, infrastructure gaps, battery degradation and regulatory hurdles continue to keep BEV market share below the government’s ZEV Mandate targets."

“Unlocking growth in BEV sales will be critical for the industry going forward, as manufacturers pursue regulatory compliance, and the UK continues to ramp up its net zero efforts. Incentivising both consumers and businesses to purchase EVs in the near term will be pivotal, but this is easier said than done given the complex landscape and persistent consumer sentiment concerns.”

Kemp concluded with a warning that the sector’s long-term future rests on navigating an increasingly complex strategic environment. “Developing a long-term strategy that delivers sustainable profitability is becoming increasingly challenging as manufacturers, suppliers and dealers address the impact of trade, geopolitics, regulation, penalties, incentives, consumer demand, product portfolio, footprint strategy and skills.

"The destination will continue to evolve but the journey will have many twists and turns.”

Login to continue reading

Or register with AM-online to keep up to date with the latest UK automotive retail industry news and insight.

Sponsorship is a great way of reaching people working in the sector as well as the wider business community right across the UK. That's why we pay very close attention to making sponsorship good value for all of our supporters. A principal benefit is that it associates your organisation with an event that is successful, creative, dynamic, well established and greatly respected.

The AM Awards offers a variety of sponsorship opportunities and advertising packages.

FIND OUT MOREAuthor:

Aimee Turner

Deputy editor

AM deputy editor Aimée Turner has been a specialist B2B editor and journalist covering the international transportation sector for more than 20 years.

She has specialised in the significant safety, regulatory, and environmental issues that impact advanced technology businesses in the pursuit of more efficient, safer and sustainable transportation modes.

Login to comment

Comments

No comments have been made yet.